Investing in China: Weighing the Risks and Opportunities

The prominence of risk-focused China coverage in business and political news has weighed heavily on investor sentiment towards Chinese equities. Many of these stories are sober, balanced assessments but others, as characterized by Ian Bremmer of the political risk consulting firm Eurasia Group are “`ideologically freighted’, advanced by those with an adversarial world view who ignore the country’s continued growth and the fact that American businesses are interested in Chinese markets.”1 This type of coverage has reaffirmed already skeptical views and deepened pessimism.

In this article, we will address three broad categories of China-specific investment risk, detailing how we think about and mitigate these risks in our portfolios:

Geopolitical Tensions

Are the U.S. and China destined to fall into “Thucydides’ Trap” and an armed conflict? Recent history and economic interdependence offer reasonable doubt.

MORE>Economic Growth

Is China the next Japan? Adverse demographic trends and high debt levels don’t paint a full picture of potential future relative strength.

MORE>Regulatory Tightening

Will China’s closed regulatory fist relax to become a new guiding hand for growth? Recent actions seem to suggest so.

MORE>

Chautauqua Capital: We Invest in Companies, not Countries.

Our investment philosophy lays out our investment criteria:

(1) companies exposed to a durable, long-term growth trend, which (2) possess competitive advantages that enable them to capture the lion’s share of the profit pool created by that trend, and (3) can be purchased at a reasonable valuation in the context of their growth outlooks and competitive positioning.

While our primary focus is at the company-level – assessing long-term growth potential and durability of competitive advantage – we do take country-level fundamentals and risks into account. A key step in our investment process is to develop a comprehensive geographic footprint of where our companies generate revenue to assess if we are taking on any undue political, economic, and regulatory risks.

The most important thing to keep in mind as you think about these risks is the fact that we invest in companies, not countries. The Chinese companies in our portfolio are growth franchises that objectively meet our stringent investment criteria.

China, the country, may be viewed in terms of geopolitical tensions, structurally slowing growth and high debt, but our Chinese companies share none of those characteristics as they are exposed to secular growth areas of the domestic economy (private consumption and healthcare) that align with government priorities, have strong balance sheets and resilient cash flows, and are not reliant on restricted Western technology inputs for future growth. We continue to be encouraged by the fundamental performance of our Chinese companies. Being cautious in China, the country, but bullish on the long-term prospects for our Chinese portfolio companies is not the dichotomy it might seem.

For more information on portfolio positioning or to be added to our email list, please contact us.

Risk Factor 1: Geopolitical Tensions

Humility is our number one cultural value at Chautauqua, so it is with a high degree of trepidation that we offer a view on the future trajectory of the U.S.-China relationship as there are far better-informed sources at the State Department, Pentagon and foreign-policy think tanks. The scenarios under consideration range from the worst case of armed conflict over Taiwan to the best case of continued, gradual economic decoupling.

To reduce potential bias, one of the features of our research process -- especially in the context of forecasting -- is to incorporate the outside view. We find a group of situations or reference class that is broad enough to be statistically significant but narrow enough to be useful in analyzing the decision we face.2 We use the outside view to “reality check” our forecasts of company fundamentals by asking questions like “how many companies in this industry or any other industry, for that matter, ever achieved and sustained the growth rates projected?” Similarly, we can use the outside view to assess the unthinkable: an armed conflict between the U.S. and China.

In 12 of 16 past cases in which a rising power (currently China) has confronted the dominant power (U.S.), the result has been war.3 Historians have named this power dynamic “Thucydides’ Trap”. Seventy-five percent probability is not a comforting baseline, nor does it say anything of the costs of a conflict and its timing,4 but this is the point in the process where we apply specific circumstances of the U.S.-China relationship to adjust the baseline probability.

The Cold War stands as one of history’s greatest successes in escaping Thucydides’ Trap. Historians have offered various explanations for why the Cold War never turned hot. Most credit the threat of nuclear mutually assured destruction (MAD), while some emphasize the geographic distance between the U.S. and the U.S.S.R., or the advent of satellite and electronic reconnaissance programs that minimized the likelihood of dangerous misunderstandings.5 Each of these mitigating factors is also present in the current U.S.-China dynamic.

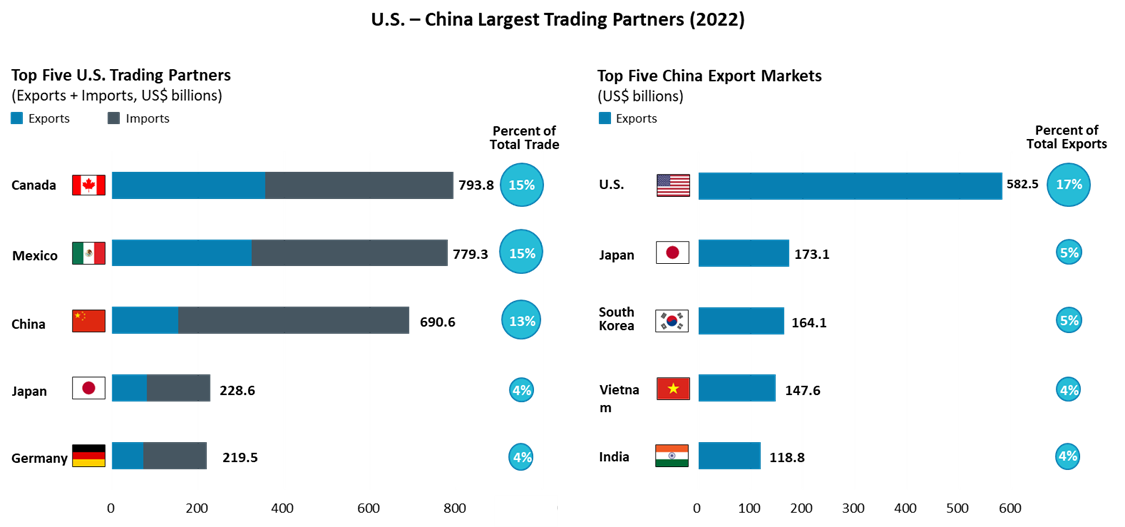

A mitigating factor absent in the Cold War case is an analog of MAD known as “MAED” – mutually assured economic disruption.6 Trade between the U.S. and the Soviet Union averaged only ~ 1% of total trade for both countries through the 1970s and 1980s, whereas U.S.-China economic relations have become very interdependent, perhaps inextricably so.7 Trade between the U.S. and China was $691 billion in 2022, accounting for 13% of total U.S. trade.8 The U.S. imports more goods from China than from any other country and China is the third largest export market for U.S. goods, supporting one million jobs.9 The U.S. is by far China’s largest export market, nearly equivalent to China’s combined exports to Japan, South Korea, Vietnam and India.10 Expanding the bilateral conflict to a multilateral one (China vs Advanced Democratic Economies11) significantly raises the economic stakes from a Chinese perspective.

Taiwan has long been a flashpoint in U.S.-China relations and is the likely epicenter of a future conflict. Yet, ironically, Taiwan itself could serve as another mitigating factor. Taiwan’s importance in the global semiconductor supply chain and China’s dependence on it has been called the island’s “silicon shield” against a Chinese attack. In 2020, China imported more than $350 billion worth of semiconductors, more in dollar terms than its imports of oil.12 More than 90% of semiconductors used in China were imported or manufactured locally by foreign suppliers, none more critical than Taiwan.13 While Taiwan’s semiconductor industry has significant strategic value, it is also a powerful reason for Beijing to refrain from attack. Assuming Taiwanese forces were to be overwhelmed during an invasion, it is unlikely that they would leave the country’s fabs (semiconductor fabrication plants) intact.14 Moreover, the key personnel required to run the fabs would be among the first to be evacuated. Keeping the world’s most advanced fabs intact and running is in the interests of everyone as the chips produced in Taiwan are present in nearly every type of electronic device used daily around the world.

Mitigating factors aside and speaking purely from an investing perspective, the potential economic costs (not to mention the human tragedy) of an armed conflict are so high as to make the risk practically undiversifiable from an equities perspective. In the context of the anticipated resulting market drawdown, a global equity portfolio that excluded Chinese stocks would likely fare only marginally better than one that had exposure to Chinese equities.

The Taiwan Strait is the primary route for ships passing from China, Japan, South Korea, and Vietnam to global markets, carrying goods from Asian factory hubs to markets in Europe, the U.S., and all points in between. According to Bloomberg, almost half of the global container fleet and 88% of the world’s largest ships by tonnage passed through the waterway in 2022.15 Nikkei Asia estimates that a war across the Taiwan Strait would destroy world trade worth $2.6 trillion (about $8,000 per person in the U.S.). UK Foreign Secretary, James Cleverly, warned that distance would offer no protection to the inevitable catastrophic blow to the global economy as “no country could shield itself from the repercussions of a war in Taiwan.”16 The RAND Corporation estimated that a one-year war between the U.S. and China would cut U.S. GDP by 5-10% and Chinese GDP by 25-35%.17 For context, U.S. GDP fell by 4.3% in real terms during the Great Recession, which was the deepest recession since World War II.18

If China decides to attack Taiwan, strategic surprise would be the first casualty due to the sheer scale of the undertaking. According to the Carnegie Endowment for International Peace “any invasion of Taiwan will not be secret for months prior to Beijing’s initiation of hostilities” as China “would take visible steps to insulate its economy, military and key industries from disruptions and sanctions.”19 From a risk management and asset allocation perspective, this would give time for investors to adapt to the increased risks. The Center of Strategic and International Studies has published economic indicators of approaching risk of conflict that include imposition of stronger cross-border capital controls, a suspension of key exports such as critical minerals and refined petroleum products, rapid liquidation and repatriation of Chinese-owned assets held abroad and restrictions on outward travel for Chinese elites or high priority workers.20 Our investment team monitors these indicators as well as others (for example, spikes in Taiwan credit default swaps, shipping insurance premiums and important political events such as the upcoming Taiwanese presidential election in January 2024) to gauge risk levels and act accordingly.

Scenarios short of an outright conflict fall into the broad category of economic decoupling which will present growth and profitability challenges for most companies. The International Monetary Fund (IMF) estimates that economic decoupling between China and the West could cost anywhere between a manageable 0.2% of global GDP and a material 7%21 – equivalent to the combined annual output of Germany and Japan, or roughly $7 trillion.22 There will be pressure on profitability as companies will have to incur incremental costs and increase capital spending to reduce their dependency on China in their supply chains. More severe scenarios incorporate negative growth impacts from higher tariffs, denial of market access, and higher regulatory compliance costs.

At a high level, we believe that our portfolio is well-positioned in an environment where growth and margins are challenged by the effects of economic decoupling. Our investment philosophy emphasizes businesses that benefit from secular growth trends and have durable competitive advantages, which often manifest themselves in the form of pricing power that should enable them to better pass-through incremental supply chain costs and protect margins relative to their competitors.

Risk Factor 2: Economic Growth

The optimism over the prospects of a Chinese economic rebound that accompanied the lifting of the government’s Zero-COVID policy at the end of last year has given way to deep pessimism. China’s recovery is faltering, and the long-term growth outlook is slowing markedly relative to the 9% average annual GDP growth rates achieved over the past two decades given the headwinds from demographics, debt, and economic decoupling from the West.

In 2022, China’s population declined for the first time in six decades. China’s total fertility rate dropped to a record low of 1.09 in 2022 from 1.30 in 2020 and is now even lower than Japan’s, a country long known for its aging society.23 China’s ongoing demographic transition constitutes a significant constraint on economic growth. A working-age population that peaked in 2011 at more than 900 million is projected to decline by over 20% to 700 million by 2050. These workers will have to provide for nearly 500 million Chinese aged 60 and over, compared with 200 million today.24 Higher age dependency ratios will place additional pressure on productivity growth, which has been slowing for two decades. From the 1980s to the early 2000s, labor productivity gains contributed one-third of China’s GDP growth. Over the past decade, that contribution has fallen to one-sixth.25

Since the Global Financial Crisis (GFC), China’s total debt (government and private) has more than doubled from 140% of GDP to close to 300%, above the 250% average for G20 nations and 220% for emerging economies.26 While the focus has been on local government financing vehicle (LGFV) and property sector debt levels, a significant share of incremental macroeconomic leverage stems from Chinese corporates taking on more debt. The average debt of companies in the Bloomberg China Large, Mid & Small Cap Index is up 87% since the end of 2016. Yet, corporate capacity to service and repay debt has fallen sharply as evidenced by free cash flow declining by 50% over the same period. According to Bloomberg, defaults in the property sector, missed payments in the wealth management industry and stress in LGFVs are all symptoms of excessive debt that is proving too tough to manage in an economy that is structurally slowing.27 While high leverage may be a characteristic of many Chinese corporates, it is important to note that all but one of our Chinese companies have net cash balance sheets and their cash flows have been more resilient in a tough macro environment.28

The main culprit for China’s economic weakness is property, which before the pandemic was a significant source of growth and is estimated to account for 29% of GDP, comparable to both Ireland and Spain before the GFC.29 The end of the long property boom has hurt the economy in multiple ways. It has dampened construction activity and all the services associated with homebuilding. A People’s Bank of China (PBoC) survey of urban households conducted in 2019 revealed that the value of housing comprised 59% of households’ total assets, while mortgage loans stood at 12% of total assets. These figures are comparable to the U.S. in 2008 on the eve of the subprime mortgage crisis and Japan in the late 1980s.30 Because homeowners are less likely to spend money if they are worried about their most valuable asset, the end of the property boom has depressed consumption. Many businesses in China use property as collateral for borrowing, so the decline in property prices has also slowed private investment.31

Economists are drawing analogies to 1990s Japan, which also had a shrinking workforce and whose growth, like China’s over the past decade and a half, was created by an investment boom, much of which was directed toward the property sector. When Japan’s real estate bubble burst in 1989 spurring a sharp drop in asset prices, growth slowed dramatically as heavily leveraged firms and households repaid their debts instead of spending on goods and services, a phenomenon known as a balance sheet recession.32

The Japan analogy has stoked fears that China could fall into a debt-deflation loop where debt to GDP keeps rising even as debt growth slows and per capital income growth stagnates. However, there are several key differences that improve China’s prospects relative to 1990s Japan.33 First, the rise in Chinese property prices was not as steep as Japan’s. China’s ratio of property values to GDP peaked at 260% of GDP after rising from 170% in 2014. In Japan, land values peaked at 560% of GDP in 1990 before falling back to 394% by 1994. Second, China still has much higher potential growth compared with Japan in the early 1990s. China’s 2022 per capital income of $12,72034 is less than 20% of the U.S. level, implying that China still has significant growth headroom. In contrast, Japan’s per capital income was nearly 20% higher than that of the U.S. in 1990.35 Finally, Chinese policy makers have the distinct advantage of learning from the mistakes of Japan whose initial policy stance was too restrictive (which led to a strong Yen and eroded the competitiveness of the corporate sector), too slow and lacked coordination of fiscal and monetary stimulus.36

The Japan analogy has stoked fears that China could fall into a debt-deflation loop where debt to GDP keeps rising even as debt growth slows and per capital income growth stagnates. However, there are several key differences that improve China’s prospects relative to 1990s Japan.33 First, the rise in Chinese property prices was not as steep as Japan’s. China’s ratio of property values to GDP peaked at 260% of GDP after rising from 170% in 2014. In Japan, land values peaked at 560% of GDP in 1990 before falling back to 394% by 1994. Second, China still has much higher potential growth compared with Japan in the early 1990s. China’s 2022 per capital income of $12,72034 is less than 20% of the U.S. level, implying that China still has significant growth headroom. In contrast, Japan’s per capital income was nearly 20% higher than that of the U.S. in 1990.35 Finally, Chinese policy makers have the distinct advantage of learning from the mistakes of Japan whose initial policy stance was too restrictive (which led to a strong Yen and eroded the competitiveness of the corporate sector), too slow and lacked coordination of fiscal and monetary stimulus.36

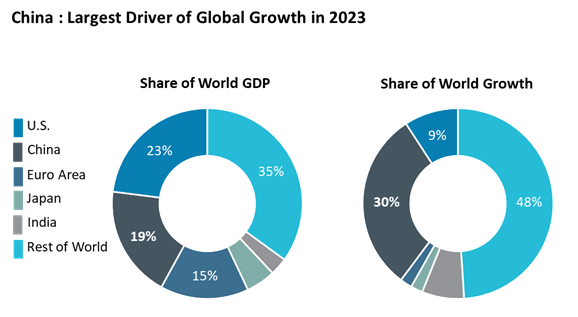

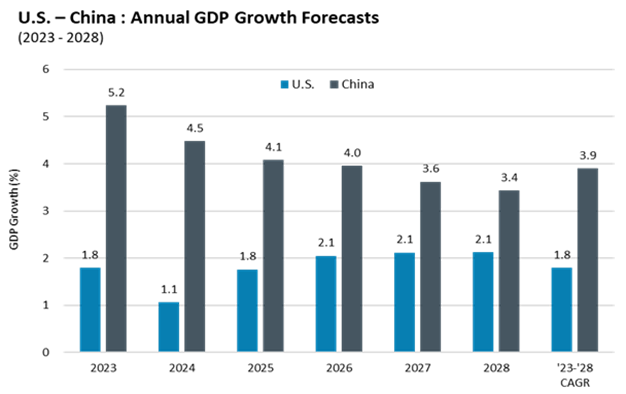

Despite the “gloomy” outlook, to put matters into perspective, China’s GDP is still forecasted to grow at twice the rate of the U.S. and remain the top contributor to global growth. The IMF projects U.S. GDP to grow at an average of 1.8% per year to 2028 while it estimates China’s GDP to average 4% annual growth over the same timeframe.37 The IMF forecasts China to account for nearly 23% of total world growth through 2028, roughly double the U.S.38 More bearish long-term forecasts show China’s real GDP growth converging to the U.S. by the end of the decade. Capital Economics, a London-based research firm, estimates that China’s trend growth has slowed to 3% from 5% in 2019 and will slow further to 2% in 2030.39

Intuitively, it makes sense to draw the conclusion that slower Chinese GDP growth bodes ill for Chinese stock performance. However, multiple academic studies have found no statistically significant relationship between a country’s economic growth and future stock returns. In fact, several studies found that low-growth countries had slightly higher average returns than high-growth countries, although this return difference was not statistically different from zero.40

In hindsight, from a top-down perspective, investing in Japan at the beginning of 1990 was the worst possible time to invest in the country (the Nikkei 225 Index is still 16% below its December 1989 peak41). First, Japan’s aging demographics and the bursting of its property bubble would soon lead to decades of sluggish growth and deflation. Second, investors buying into Japan in 1990 were paying extremely expensive valuations – more than 50x earnings – which is the key difference between 1990s Japanese and present-day Chinese equities, which trade at only 10.8x (a 43%, 35% and 17% discount to the S&P 500, World ex-China and Emerging Markets ex-China indices, respectively).42 Yet, against the dismal economic and market backdrop in Japan, it was possible for bottom-up investors to identify and invest in Japanese companies whose strong fundamentals would drive world-beating share price performance.43 One of these companies is Keyence, which meets our investment criteria, in spite of the persistent macro headwinds in its home market. Keyence has been in our portfolios since 2016.

The Bottom Line

A company’s long-term fundamentals, not its home country’s GDP growth, ultimately drive its share price performance. Stock selection, not country selection, drives our portfolios’ long-term returns.

Risk Factor 3: Regulatory Tightening

Starting with the November 2020 cancellation of the IPO for Ant Group, a financial technology firm controlled by Alibaba founder Jack Ma, the Chinese government initiated a regulatory tightening cycle unprecedented in terms of its intensity, scope, and duration. With the stated aim of fostering “common prosperity,” the government introduced regulations targeting internet platform, education, and property companies. The regulatory headwinds in China have had a tangible impact on corporate fundamentals and an even greater impact on investor sentiment as evidenced by the 50% decline in Chinese equities since their February 2021 peak, wiping out more than $1 trillion in equity market value.

For our Chinese companies, it is our assessment that new regulations introduced over the past three years should not structurally impair their earnings power. However, as in the case of our former position in TAL Education, when regulations impair the long-term earnings power of any business, we take decisive action and exit the position in accordance with our strict sell-discipline.

That said, we see signs that regulatory headwinds in China may be changing. After a freeze that lasted more than one year, regulators resumed issuing video game licenses to Tencent and NetEase in late 2022. In July, financial regulators imposed a $1 billion fine on Ant Group, ending an investigation that began in 2020. That probe was seen as the starting point in the government’s campaign to exert more control over the country’s most influential technology companies and their billionaire entrepreneur founders. The Communist Party and government issued a rare joint pledge on July 19th to improve conditions for private businesses. Beijing outlined more than 30 measures that included promises to treat private companies the same as state-owned enterprises and consult more with entrepreneurs on drafting policies and regulations. Chinese regulators met with global investors on July 21st and again on August 25th to sound out and address their lingering concerns.44

Government is a powerful force in all economies and investors are best served by aligning their exposures with government priorities. Nowhere has this been more true than in China. Two key government priorities are to foster more consumption-led growth and improve health care delivery for an aging population. Our Chinese portfolio companies are leveraged to and well-positioned to capitalize on these priorities.

China wants to increase self-reliance through its “dual circulation” strategy, which seeks to reduce exports as a primary driver of economic growth by boosting domestic consumption. The GDP share of household spending is under 40%, well-below the level of 60% or more in most Organization for Economic Co-operation and Development (OECD) economies.45 Private consumption has been resilient against the backdrop of slower economic growth. Despite the near-term uncertainties and inevitable challenges of China transitioning from investment-led to consumption-led growth, investors should not be myopic to the scale of the long-term consumption opportunity. China’s middle class currently numbers 400 million and is projected to grow by an additional 400 million by 2035, which should unleash a wave of consumer spending that would make China the largest consumer market for both domestic and foreign firms.46

Chinese spending on healthcare is also below global averages. China spends less than 6% of its GDP on healthcare versus nearly 9% of GDP for OECD countries and 17% for the U.S.47 Chinese healthcare spending has been growing faster than GDP and its share of GDP is forecast to converge toward the global average. China’s importance in the global healthcare market, both as a growing end-market and as a center of drug discovery and manufacturing, will only increase over the long-term.

For more information on portfolio positioning or to be added to our email list, please contact us.

Disclosure

Sources for all charts: International Monetary Fund, World Economic Outlook Database, April 2023 and World Economic Outlook Update, July 2023, September 2023.

This material is provided for informational purposes only and contains no investment advice or recommendations to buy or sell any specific securities. All investments carry risk and because the Chautauqua International and Global Growth equities strategies invest in foreign securities, which involve additional risks such as currency rate fluctuations and the potential for political and economic instability, and different and sometimes less strict financial reporting standards and regulations. They may also hold fewer securities than other strategies, which increases the risk and volatility because each investment has a greater effect on the overall performance. Past performance is no guarantee of future results.

This commentary represents portfolio management views and portfolio holdings as of 06/30/23. Those views and portfolio holdings are subject to change without notice. The specific securities identified do not represent all the securities purchased, sold or held for accounts and you should not assume these securities were or will be profitable.

The MSCI ACWI ex-U.S. Index®. Is a free float-adjusted market capitalization weighted index that is designed to capture large- and mid-cap stocks across 22 of 23 developed markets countries, excluding the United States, and 24 emerging markets countries. The MSCI ACWI Index® is a free float-adjusted market capitalization weighted index that is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets, including the United States. Indices are unmanaged and direct investment is not possible.

The MSCI information may only be used for your internal use, may not be reproduced, or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

For additional important information about the fees, expenses, risks and terms of investment advisory accounts at Baird, please review Baird’s Form ADV Brochure, which can be obtained from your financial advisor and should be read carefully before opening an investment advisory account.

©2023 Robert W. Baird & Co. Incorporated. First use: 09/2023

1Peak China. (2023, August 20). The New York Times.

2Mauboussin, Michael J. (2009). Think Twice: Harnessing the Power of Counterintuition (pp 1-16). Harvard Business Press.

3Allison, Graham. (2015, September 24). The Thucydides Trap: Are the U.S. and China Headed for War? The Atlantic. https://www.theatlantic.com/international/archive/2015/09/united-states-china-war-thucydides-trap/406756/

4According to the Annual Threat Assessment of the US Intelligence Community (Office of the Director of National Intelligence) published on February 6, 2023, “Beijing is working to meet its goal of fielding a military by 2027 designed to deter U.S. intervention in a future cross-Strait crisis”, p. 7; In testimony before the House Armed Services Committee on March 29, 2023, Defense Secretary Llyod Austin said in a response to questions about whether and how soon China would invade Taiwan that “I don’t think an attack on Taiwan is imminent, nor inevitable.” Source: Wadhams, N. & Trion, R. (2023, March 29). Austin Sees No Sign Chinese Invasion of Taiwan is Imminent. Bloomberg.

5Case File | Belfer Center for Science and International Affairs. (n.d.) Harvard Kennedy School – Belfer Center for Science and International Affairs. https://www.belfercenter.org/programs/thucydidess-trap/thucydidess-trap-case-file

6Allison, Graham, Kiersznowski, Nathalie & Fitzek, Charlotte. (March 2022). The Great Economic Rivalry. Harvard Kennedy School – Belfer Center for Science and International Affairs, p. 31. https://www.belfercenter.org/publication/great-economic-rivalry-china-vs-us

7Wikipedia contributors. (2023). Foreign Trade of the Soviet Union. Wikipedia https://en.wikipedia.org/wiki/Foreign_trade_of_the_Soviet_Union

8Trade defined as the sum of goods exports to China and goods imports from China. Source: Bureau of Economic Analysis (BEA) – U.S. Department of Commerce. (2023, February 7). U.S. International Trade in Goods and Services December and Annual 2022 [Press release]. https://www.bea.gov/sites/default/files/2023-02/trad1222.pdf – Note that in addition to trade in goods, U.S.-China trade in services was $68 billion in 2022. Final 2022 services trade data was released separately by the BEA on July 6, 2023.

9The US-China Business Council. (2023). US Exports to China: Goods and Services Exports to China and the Jobs They Support, by State and Congressional District, p. 1. https://www.uschina.org/reports/us-exports-china-2023-0

10Japan, South Korea, Vietnam, and India were China’s #2-#5 export markets in 2022, excluding Hong Kong. Source: IMF Direction of Trade Statistics. https://data.imf.org/?sk=9d6028d4-f14a-464c-a2f2-59b2cd424b85

11Advanced Democratic Economies (ADEs) are liberal democracies with advanced economies. ADEs defined as the Group of Seven (G7) countries – Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States – plus Australia, Norway, Republic of Korea, and the European Union. Source: Kramer, Franklin D. (February 2023). China and the New Globalization. Atlantic Council | Scowcroft Center for Strategy and Security, p. 2. https://www.atlanticcouncil.org/in-depth-research-reports/report/china-and-the-new-globalization/

12Cronin, Richard. (2022, August 16). Semiconductors and Taiwan’s “Silicon Shield.” Stimson Center. https://www.stimson.org/2022/semiconductors-and-taiwans-silicon-shield/

13Lee, Y., Shirouzu, N., & Lague, D. (2021, December 27). Silicon Fortress – T-DAY – The Battle for Taiwan. Reuters. https://www.reuters.com/investigates/special-report/taiwan-china-chips/

14Crawford, A., Dillard, J., Fouquet, H., & Reynolds, I. (2021, January 25). The World is Dangerously Dependent on Taiwan for Semiconductors. Bloomberg.

15Varley, K. (2022, August 2). Taiwan Tensions Raise Risks in One of the Busiest Shipping Lanes. Bloomberg.

16Wintour, P. (2023, April 25). If China invaded Taiwan it would destroy world trade, says James Cleverly. The Guardian. https://www.theguardian.com/world/2023/apr/25/if-china-invaded-taiwan-it-would-destroy-world-trade-says-james-cleverly

17Compert, David C., Cevallos, Astrid S. & Garafola, Cristina L. (2016). War with China: Thinking Through the Unthinkable. RAND Corporation, pp. 41-50, 85-88. https://www.rand.org/pubs/research_reports/RR1140.html; Based on the work of Reuven Glick and Alan M. Taylor, “Collateral Damage: Trade Disruption and the Economic Impact of War” (2010) which studied falls in bilateral trade between combatants and corresponding declines domestic consumption in World War I and World War II, RAND assumes that U.S.-China bilateral trade drops by 90% and domestic consumption falls by 4% in each country. A potential conflict’s GDP impact is asymmetrically higher on China as RAND assumes that China also suffers an 80% decline in East Asia regional trade and its other global trade falls by 50% because of the postulated “war zone” effect on seaborne trade in the Western Pacific (~90% of China’s trade is seaborne). The high-end of U.S. estimated GDP loss includes an anticipated decline in trade with other Asian countries due to the “war zone” effect on seaborne trade. China’s estimated 25-35% decline in GDP can compared with Germany’s 29% decline in real GDP during World War I, when Germany itself was spared heavy damage.

18Rich, B. R. (n.d.). The Great Recession. Federal Reserve History. https://www.federalreservehistory.org/essays/great-recession-of-200709#:~:text=Beyond%20its%20duration%2C%20the%20Great,data%20as%20of%20October%202013) .

19Culver, John. (2022, October 3). How We Would Know When China Is Preparing to Invade Taiwan. Carnegie Endowment for International Peace. https://carnegieendowment.org/2022/10/03/how-we-would-know-when-china-is-preparing-to-invade-taiwan-pub-88053

20DiPippo, Gerard. (2022, August 16). Economic Indicators of Chinese Military Action Against Taiwan. Center for Strategic & International Studies. https://www.csis.org/analysis/economic-indicators-chinese-military-action-against-taiwan

21America v China – It’s Worse Than You Think (2023, April 1-7). The Economist.

22Martin, E. (2023, April 6). IMF Warns Five-Year Global Growth Outlook Weakest Since 1990. Bloomberg.

23Qi, L. (2023, August 19-20). China’s Fertility Rate Dropped Sharply, Report Shows. The Wall Street Journal.

24O’Hanlon, Michael E. (2023, April 24). China’s Shrinking Population and Constraints on Its Future Power. Brookings. https://www.brookings.edu/articles/chinas-shrinking-population-and-constraints-on-its-future-power/

25Wei, L., & Xie, S. Y. (2023, August 21). China’s 40-Year Boom Is Over Raising Fears of Extended Slump. The Wall Street Journal.

26Bloomberg Economics. (2023, August 21). CHINA INSIGHT: Rescue – Or Risk Crisis on Debt Too Big to Manage. Source: Bloomberg.

27IBID.

28Our sole holding with net debt had a Net Debt/EBITDA ratio of 0.58x at the end of 2022. Source: Bloomberg.

29Liu, Z. Z., & Stemp, D. (2023, March 21). The PBoC Props Up China’s Housing Market. Council on Foreign Relations. https://www.cfr.org/blog/pboc-props-chinas-housing-market#:~:text=Kenneth%20Rogoff%20estimated%20that%20the,before%20the%20global%20financial%20crisis

30IBID

31Confidence Trap. (2023, June 24-30). The Economist.

32IBID

33Ahya, Chetan. (2023, August 8). How China could avoid a 1990s Japan situation. Morgan Stanley Research.

34Source: The World Bank.

35Ahya, Chetan. (2023, August 8).

36Alloway, T., & Weisenthal, J. (2023, July 10). Richard Koo Is Getting Famous in China as Debt Problems Grow. Bloomberg.

37International Monetary Fund. (April 2023). World Economic Outlook.

38Tanzi, A. (2023, April 17). China to Be Top World Growth Source in Next Five Years, IMF Says. Bloomberg.

39Wei, L., & Xie, S. Y. (2023, August 21). China’s 40-Year Boom Is Over Raising Fears of Extended Slump. The Wall Street Journal.

40Swedroe, Larry. (2022, October 5). Is There a Link Between GDP Growth and Emerging Market Returns. The Evidence Based Investor (TEBI).

41Nikkei 225 Index peaked on December 29, 1989, at 38,916. On August 31, 2023, the Nikkei 225 Index closed at 32,619. Source: Bloomberg.

4212-month forward PE for the Bloomberg China Large-Mid Index (CN), S&P 500 Index (SPX), Bloomberg World ex-China Index (WORLDXC) and Bloomberg Emerging Markets ex-China (EMXCN) as of 8/31/23. CN Index 12-month forward PE discounts relative to the SPX, WORLDXC and EMXCN indices are at the high-end of their historical ranges since December 2009 – 98th, 88th and 87th percentiles, respectively. Source: Bloomberg.

43From December 29, 1989, to August 31, 2023, in U.S. dollar terms, Keyence’s total return of 5,227% (12.5% annualized) compares to a total return of 2,451% (10.1% annualized) for the S&P 500. Source: Bloomberg.

44Huang, Z., Zhang, J. and Zheng, S. (2023, July 24). China’s Tech Crackdown is Ending. What Does It Mean? Bloomberg; (2023, August 25). Everything China Is Doing to Juice Its Flagging Economy. Bloomberg.

45Huang, T., & Lardy, N. (2023, January 10). Can China revive growth through private consumption? Peterson Institute for International Economics. https://www.piie.com/blogs/realtime-economics/can-china-revive-growth-through-private-consumption

46Allison, Graham, Kiersznowski, Nathalie & Fitzek, Charlotte. (March 2022). The Great Economic Rivalry. Harvard Kennedy School – Belfer Center for Science and International Affairs, p. 42.

47Health spending as percent of GDP by country | TheGlobalEconomy.com. https://www.theglobaleconomy.com/rankings/health_spending_as_percent_of_gdp/