May 2026 Bond Market Comments

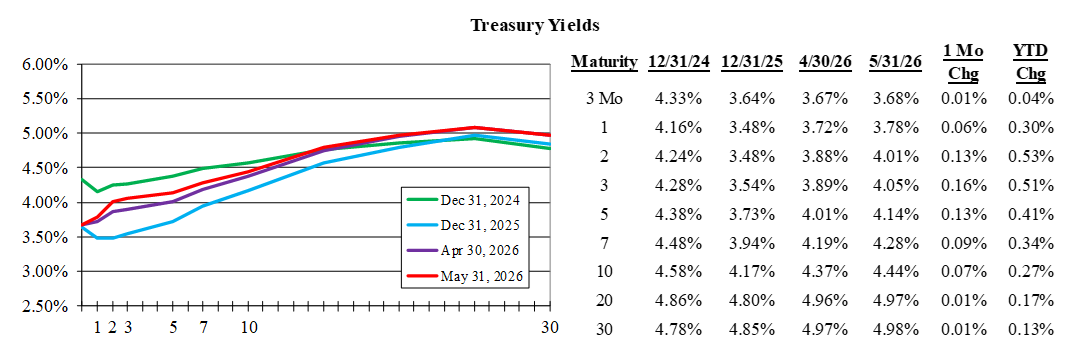

Treasury Yields Rise and Curve Flattens as Inflation Concerns Persist; Warsh Confirmed as 17th Fed Chair

The upward trend in Treasury yields, which coincides with the late February onset of the Iran conflict, continued in May as the 10yr Treasury rose another 7 bps to 4.44%. The 2yr Treasury rose 13 bps, leaving 2s10s spread at 43 bps, its flattest reading since last summer. The large rise in short yields was a byproduct of markets continuing to shift from pricing rate cuts in late 2026 to now assigning increased probability of a hike. Inflation concerns, driven in large part by elevated oil prices hovering around $100/barrel due to the ongoing closure of the Strait of Hormuz, were evident as the 30yr Treasury reached 5.18% intramonth, its highest level since 2007, before settling at 4.98% by month end. April core PCE inflation of 3.3% YoY matched expectations but was also its highest YoY reading since 2023. The “vast majority” of Fed officials noted in meeting minutes increased risk that inflation would take longer to get to their 2% target than previously expected. The labor market remained steady as +115k payrolls were reported in April with a low and steady unemployment rate of 4.3%. Kevin Warsh was sworn in as the 17th Federal Reserve Chair on May 22 following a 54-45 Senate confirmation. His first meeting as Chair is June 16–17; markets assign a near-zero probability of a rate move at that meeting.

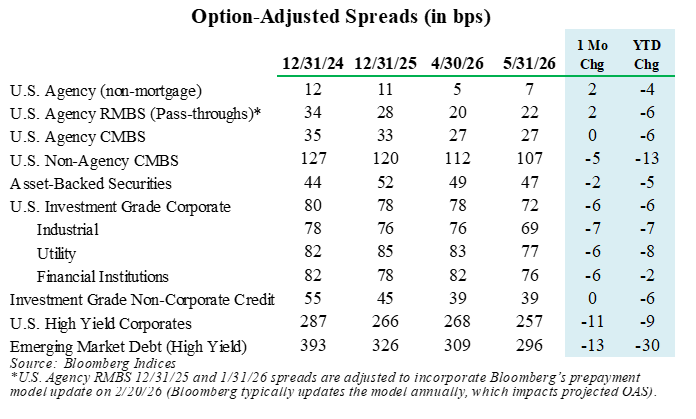

High Absolute Yields Foster Tighter Spreads

Spreads tightened further as capital flowed into the U.S. bond market in response to higher absolute yields. Early estimates peg May’s industry bond fund inflows as the strongest month in over 15 years. U.S. IG Corporate spreads closed at +72 bps, just 1 bp above the recent tight reached in January, which represented a 28-year tight in spreads. Non-Agency CMBS and ABS tightened in sympathy as well.

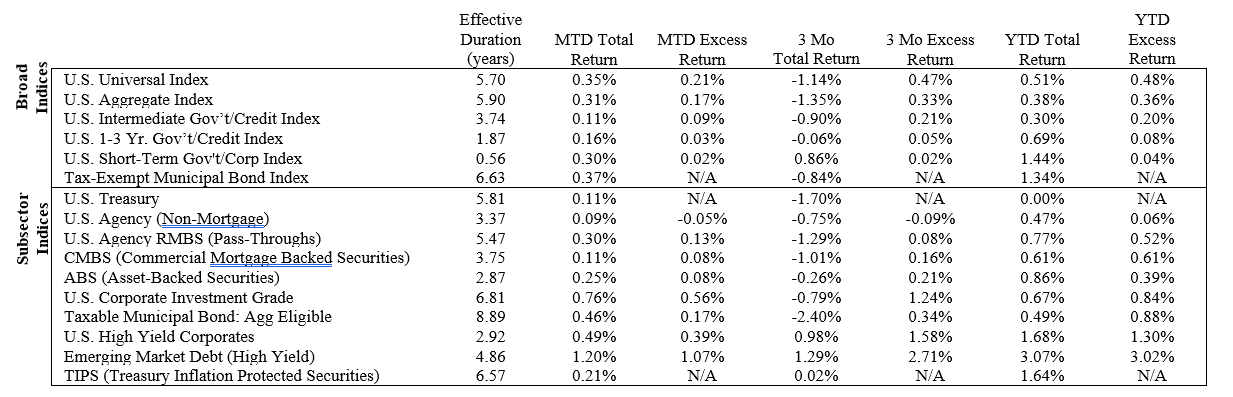

Excess Returns Positive Across Spread Sectors

The Agg Index returned 0.31% in May, lifting YTD results to 0.38%. IG sector total and excess returns were led by IG Corporates at 0.76% and 0.56%, respectively. Only EM High Yield produced higher total and excess returns for the month among major subsectors. Tax-exempt municipals outperformed Treasuries in May.

Returns of Selected Bloomberg Indices and Subsectors

*Excess return represents the return of a spread sector versus a like-duration U.S. Treasury.

Disclosures

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. This is not a complete analysis of every material fact regarding any company, industry or security. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Past performance is not a guarantee of future results.

Fixed income is generally considered to be a more conservative investment than stocks, but bonds and other fixed income investments still carry a variety of risks such as interest rate risk, credit risk, inflation risk, and liquidity risk. In a rising interest rate environment, the value of fixed- income securities generally decline and conversely, in a falling interest rate environment, the value of fixed-income securities generally increase. High yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield.

Treasury yields are the interest rates that the U.S. government pays to borrow money for varying periods of time.

Option-adjusted spread is the difference between the yield of a security that pays fixed interest payments and the current U.S. Treasury rates, which represents the rate of return on a risk-free investment.

The Bloomberg U.S. Aggregate Bond Index is an index comprised of approximately 6000 publicly traded bonds including U.S. Government, mortgage-backed, corporate, and Yankee bonds with an average maturity of approximately 10 years.

The Bloomberg Government/Credit Index is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt.

The Bloomberg Intermediate U.S. Government/Credit Bond Index is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt with maturities between one and ten years.

The Bloomberg 1-3 Year U.S. Government/Credit Bond Index is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt with maturities between zero and three years.

The Bloomberg U.S. Treasury Index includes public obligations of the U.S. Treasury. Treasury bills are excluded by the maturity constraint of at least one year but are part of a separate Short Treasury Index. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded. STRIPS are excluded from the index because their inclusion would result in double- counting. Securities in the Index roll up to the U.S. Aggregate, U.S. Universal, and Global Aggregate Indices. The U.S. Treasury Index was launched on January 1, 1973.

U.S. Agency: This index is the U.S. Agency component of the U.S. Government/Credit index. Publicly issued debt of U.S. Government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the U.S. Government (such as USAID securities). The largest issues are Fannie Mae, Freddie Mac, and the Federal Home Loan Bank System (FHLB). The index includes both callable and non-callable agency securities.

U.S Corporate – Investment Grade: This index is the Corporate component of the U.S. Credit index. It includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

CMBS (Commercial Mortgage-Backed Securities): This index is the CMBS component of the U.S. Aggregate index. The Bloomberg CMBS ERISA-Eligible Index is the ERISA-eligible component of the Bloomberg CMBS Index. This index, which includes investment grade securities that are ERISA eligible under the underwriter’s exemption, is the only CMBS sector that is included in the U.S. Aggregate Index.

MBS (Mortgage-Backed Securities): This index is the U.S. MBS component of the U.S. Aggregate index. The MBS Index covers the mortgage- backed pass-through securities of Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The MBS Index is formed by grouping the universe of over 600,000 individual fixed rate MBS pools into approximately 3,500 generic aggregates.

ABS (Asset-Backed Securities): This index is the ABS component of the U.S. Aggregate index. The ABS index has three subsectors: credit and charge cards, autos, and utility. The index includes pass-through, bullet, and controlled amortization structures. The ABS Index includes only the senior class of each ABS issue and the ERISA-eligible B and C tranche. The Manufactured Housing sector was removed as of January 1, 2008, and the Home Equity Loan sector was removed as of October 1, 2009.

Corporate High Yield: The Bloomberg U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. Original issue zeroes, step-up coupon structures, 144-As and pay-in-kind bonds (PIKs, as of October 1, 2009) are also included.

Emerging Market: Bloomberg uses a fixed list of countries defined as emerging markets countries for index inclusion purposes that is based on World Bank Income group definitions (Low/Middle), IMF country classifications (Non-Advanced Economies), and other advanced economies that may be less accessible or investable for global debt investors.

The Bloomberg Municipal Bond Index is a broad-based, total-return index. The bonds are all investment-grade, tax-exempt, and fixed-rate securities with long-term maturities (greater than 2 years). They are selected from issues larger than $50 million.

The Bloomberg TIPS Index consists of Treasury Inflation Protected Securities (TIPS). TIPS are securities whose principal is tied to the Consumer Price Index. TIPS pay interest semi-annually, based on the fixed rate applied to the adjusted principal.

Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment grade investments are those rated from highest down to BBB- or Baa3.

This is not a complete analysis of every material fact regarding any company, industry or security. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Indices are unmanaged and are not available for direct investment.

©2026 Robert W. Baird & Co. Incorporated.