June 2026 Municipal Market Comments

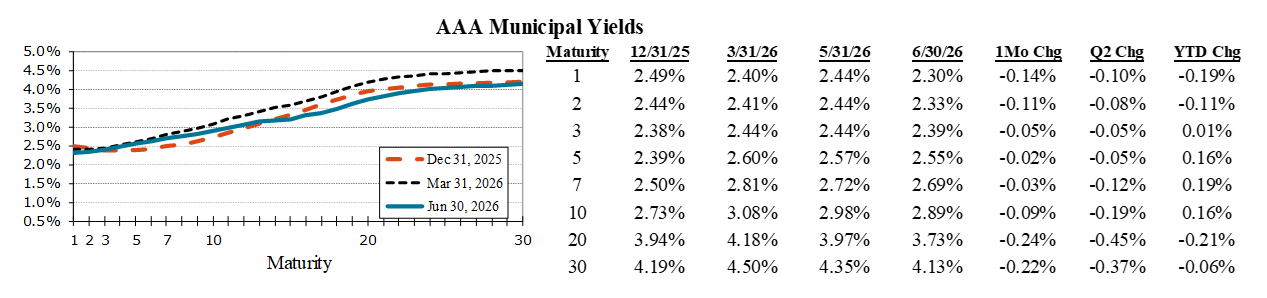

Tax-Exempt Yields Fall Amid Strong Demand

Tax-exempt yields declined in June, led by the very short end and long end of the curve. For the quarter, however, the move was driven primarily by long-end strength, with 30yr yields falling 37 bps compared to a more modest 5 bps decline in 5yr yields. As a result, the yield curve flattened, with the spread between 2yr (2.33%) and 30yr (4.13%) maturities narrowing to +180 bps at quarter-end, down from +209 bps at the end of the first quarter. Despite this flattening trend, the curve remains relatively steep, particularly as measured against the Treasury curve, and continues to offer opportunities for investors to capture incremental yield and roll-down return further out the curve. Market performance was supported by strong investor demand, as municipal bond funds recorded inflows in 12 of 13 weeks during the quarter. Net inflows totaled $10.2B in June and approximately $50B YTD, providing consistent support to absorb elevated issuance. Municipals also benefited from periods of heightened volatility in the Treasury market, driven by geopolitical developments and a more hawkish tone from the Federal Reserve, which contributed to relative outperformance versus Treasuries. New-issue supply remained robust, with June tax-exempt issuance totaling $68B, up 6.2% YoY. YTD tax-exempt issuance has reached $275B, representing a 7.3% increase over 2025’s record pace. Favorable summer technicals, driven by elevated principal and interest reinvestment flows, are expected to persist through July and August and should continue to provide support for the asset class in the near term.

Municipal Housing Bonds

Recent federal policy developments have brought renewed focus to the municipal housing sector, highlighted by Congressional passage of the 21st Century Road to Housing Act, which aims to address ongoing affordability challenges. While the legislation is not expected to materially alter the municipal market in the near term, it underscores the growing policy emphasis on expanding housing supply at a time when affordability remains a central issue nationally. Within the municipal market, housing represents a significant and well-established revenue sector, totaling roughly $335B outstanding (about 8% of the municipal market) across single-family and multifamily programs and characterized by generally high credit quality, with bonds in the broad index averaging in the AA+ category. These credit fundamentals are supported by the presence of state and local housing finance authorities, strong structural protections, federal program support, and diversified loan pools. Housing issuance trends have remained constructive in recent years and are expected to continue expanding, driven by persistent demand for affordable housing. Looking ahead, recent changes passed in the OBBB, which increase the availability of Low-Income Housing Tax Credits, are likely to further support development activity and contribute to incremental growth in municipal housing supply. Against this backdrop, housing remains an important and resilient component of the municipal landscape, reinforcing the longer-term role of municipal finance in supporting housing development and helping address supply constraints across the country.

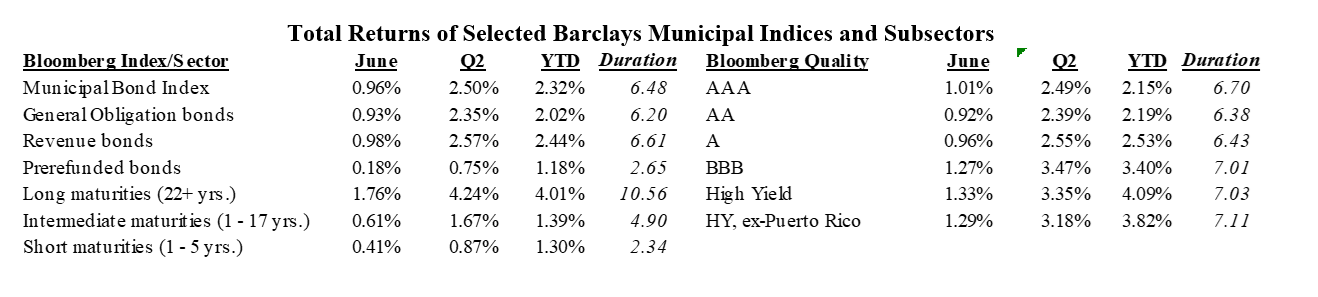

Positive QTD and YTD Returns

Returns were positive for the month, quarter, and YTD periods. Performance was led by long-duration bonds, as yields declined most significantly at the long end of the curve. Revenue issues outperformed both GOs and Prerefunded issues for the quarter and YTD. Lower-rated bonds also led returns, with securities rated BBB leading higher-quality counterparts. High Yield continued to outperform Investment Grade.

Disclosures

Fixed income is generally considered to be a more conservative investment than stocks, but bonds and other fixed income investments still carry a variety of risks such as interest rate risk, credit risk, inflation risk, and liquidity risk. In a rising interest rate environment, the value of fixed-income securities generally decline and conversely, in a falling interest rate environment, the value of fixed-income securities generally increase. High yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield.

The Bloomberg Municipal Bond Index is a broad-based, total-return index. The bonds are all investment-grade, tax-exempt, and fixed-rate securities with long-term maturities (greater than 2 years). They are selected from issues larger than $50 million. The components listed below the Municipal Bond Index (long maturities, intermediate maturities, short maturities, prefunded bonds, general obligation bonds and revenue bonds) are subsectors of the Bloomberg Municipal Bond Index and do not represent separate indices.

The Bloomberg High Yield Municipal Index includes bonds with a par value of at least $3 million and must be issued as part of a transaction of at least $20 million. The maximum rating for inclusion is Ba1/BB+/BB+ using the middle rating.

For more information about the Bloomberg Municipal Bond Index or Bloomberg High Yield Municipal Index, please visit https://www.bloomberg.com/professional/products/indices/documentation/?currentPage=1

Municipal securities investments are not appropriate for all investors, especially those taxed at lower rates. The alternative minimum tax (AMT) may be applicable, even for securities identified as tax exempt. Past performance is not a guarantee of future results.

Ratings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest). Investment grade investments are those rated from highest down to BBB- or Baa3.

Robert W. Baird & Co. Incorporated.

This is not a complete analysis of every material fact regarding any company, industry or security. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Indices are unmanaged and are not available for direct investment.